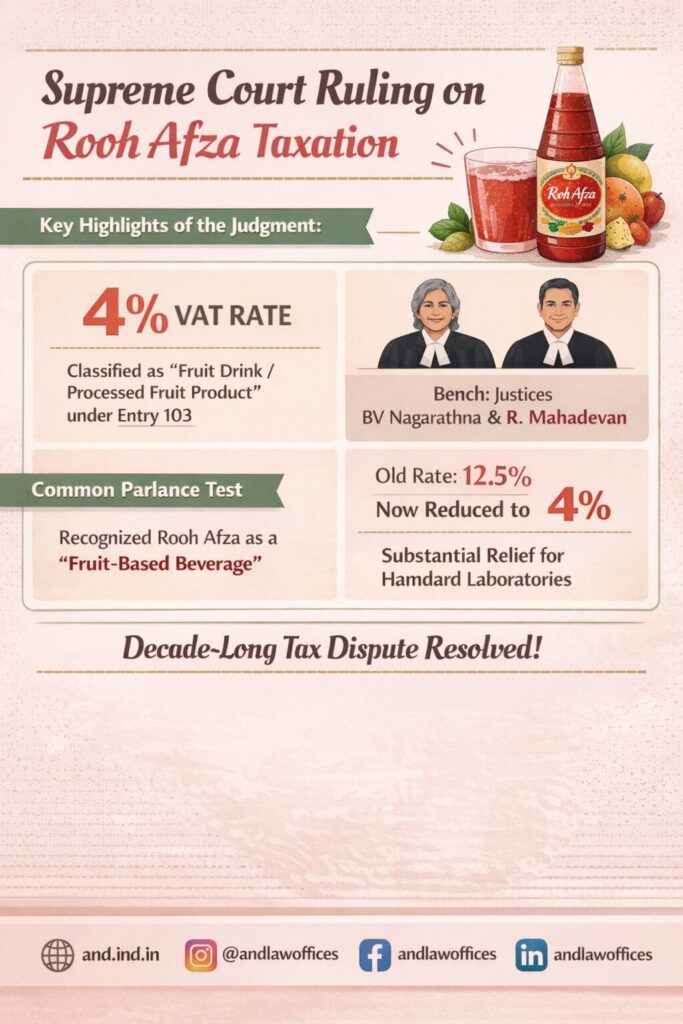

In a significant judgment, the Supreme Court of India resolved a long-standing tax dispute concerning the classification of “Sharbat Rooh Afza” under the Uttar Pradesh Value Added Tax Act, 2008. The Court held that Rooh Afza qualifies as a “fruit drink/processed fruit product” under Entry 103, thereby attracting a lower 4% VAT rate, instead of the previously imposed 12.5% rate for the period between 2008 and 2012.

Background of the Dispute

The case arose from a disagreement over how Rooh Afza should be classified for taxation purposes. The authorities had earlier treated the product as an “unclassified item”, which attracted a higher tax rate of 12.5%. This classification led to a prolonged dispute involving Hamdard Laboratories, the manufacturer of Rooh Afza.

The central issue before the Court was whether Rooh Afza should be taxed as a general unclassified product or as a fruit-based beverage falling under a specific category.

Supreme Court’s Decision

The bench comprising Justices B.V. Nagarathna and R. Mahadevan rejected the classification of Rooh Afza as an unclassified item. The Court held that the product should instead be categorized under Entry 103 as a fruit drink or processed fruit product, making it eligible for the lower tax rate of 4%.

This decision effectively overturned the earlier interpretation and brought clarity to the product’s tax treatment.

Basis of Classification

A key reasoning adopted by the Court was that Rooh Afza derives its essential character as a beverage from fruit-based extracts, even though it contains a significant proportion of sugar syrup. The Court emphasized that the presence of sugar does not alter the fundamental nature of the product as a fruit-based drink.

Thus, the classification was based on the overall character and composition of the product rather than a narrow or technical interpretation.

Application of the Common Parlance Test

An important principle applied by the Court was the “common parlance test.” According to this approach, the classification of goods for taxation should align with how they are understood by consumers in everyday usage.

The Court noted that consumers generally perceive Rooh Afza as a fruit-based beverage, not as an undefined or miscellaneous product. Therefore, the tax classification must reflect this common understanding rather than rely solely on rigid technical definitions.

Tax Implications of the Judgment

The ruling has significant financial implications. By classifying Rooh Afza under Entry 103, the applicable tax rate is reduced from 12.5% to 4%, resulting in substantial relief for the manufacturer.

Additionally, the judgment resolves a decade-long dispute concerning the tax liability for the period between 2008 and 2012, providing clarity and certainty in the application of VAT laws.

Conclusion

This judgment highlights the importance of adopting a practical and consumer-oriented approach in tax classification. By relying on the common parlance test and recognizing the essential nature of the product, the Supreme Court ensured a fair and logical interpretation of tax laws.

The ruling not only settles a long-pending dispute but also sets a precedent for future cases, emphasizing that taxation must align with real-world understanding rather than purely technical categorization.